10 Portfolio Optimization Techniques to Master in 2025

Explore 10 powerful portfolio optimization techniques. Learn how to apply methods like MPT, Risk Parity, and more to build a smarter, more resilient portfolio.

Stop throwing darts and start building a portfolio with intention. In today's complex markets, relying on gut feelings or outdated rules of thumb is a recipe for missed opportunities and unnecessary risk. The secret to durable, long-term growth lies in a disciplined, mathematical approach. This guide demystifies the world of professional investment management, breaking down 10 powerful portfolio optimization techniques used by top-tier asset managers.

We'll move beyond the theory and dive into the practical mechanics of each method, exploring how they work and how you can apply their principles. This is not a high-level overview, it's a practical roadmap for implementation.

You will learn how to:

- Balance risk and return using foundational models like Mean-Variance Optimization.

- Incorporate your market views with sophisticated methods like the Black-Litterman model.

- Build all-weather portfolios by focusing on risk contribution through Risk Parity.

- Hedge against worst-case scenarios using advanced strategies like Conditional Value at Risk (CVaR).

Whether you're a long-term stock investor, a crypto asset holder, or simply a risk-conscious planner, mastering these strategies provides the tools to construct a more resilient and efficient portfolio. This article will equip you with specific, actionable insights to move beyond guesswork and start making mathematically sound investment decisions. We will explore everything from Minimum Variance and Factor-Based investing to the Kelly Criterion, providing a comprehensive toolkit for building a smarter portfolio designed to weather market storms and capture sustainable growth.

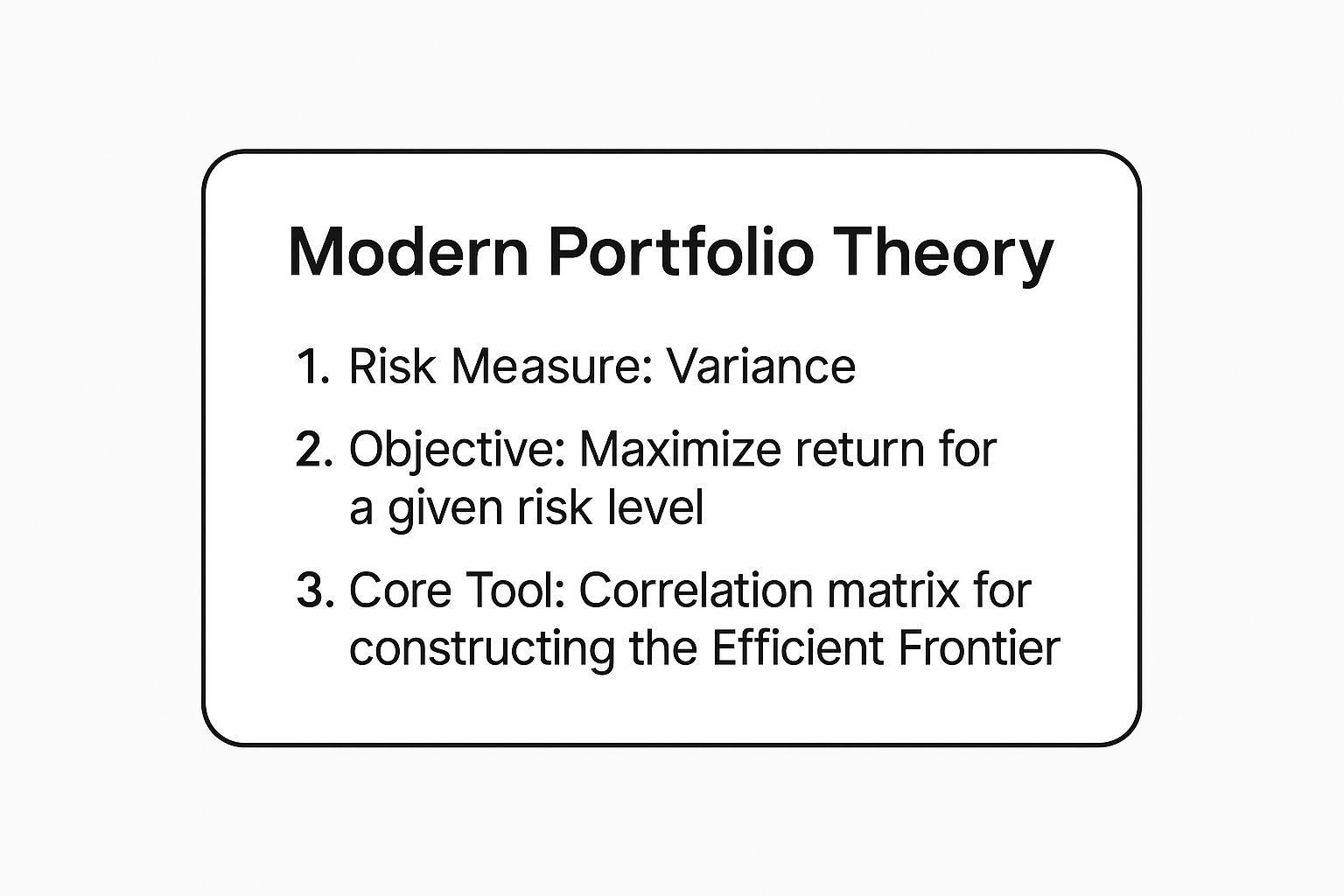

1. Modern Portfolio Theory (Mean-Variance Optimization)

Modern Portfolio Theory (MPT), pioneered by Nobel laureate Harry Markowitz, is a cornerstone of modern finance and one of the most foundational portfolio optimization techniques. It provides a mathematical framework for assembling a portfolio of assets to maximize expected return for a given level of risk. The core idea is that an asset's individual risk and return characteristics should not be viewed in isolation; instead, its contribution to the overall portfolio's risk and return is what truly matters.

MPT operates on the principle that diversification can reduce portfolio risk without sacrificing potential returns. By combining assets that are not perfectly positively correlated, the volatility of the entire portfolio can be smoothed out. The framework uses historical data for asset returns, variances (a measure of risk), and correlations to plot what is known as the "Efficient Frontier." This is a curve representing all possible portfolios that offer the highest expected return for each level of risk.

When to Use This Approach

This technique is ideal for long-term investors who aim to build a diversified portfolio and are comfortable relying on historical statistical measures. It's particularly effective for constructing foundational portfolios across traditional asset classes like stocks and bonds. Major robo-advisors such as Betterment and Wealthfront, along with institutional products like Vanguard's Target Date Funds, build their allocation strategies on MPT principles, demonstrating its widespread applicability and success.

The following summary box highlights the core components of this widely adopted framework.

As the visualization shows, MPT's objective is to achieve optimal diversification by carefully analyzing how assets move in relation to one another.

Actionable Implementation Steps

To effectively apply Modern Portfolio Theory, consider the following best practices:

- Gather Robust Inputs: The quality of your optimization depends heavily on your input data. Use reliable, long-term historical data for returns, standard deviations, and correlations.

- Apply Constraints: To avoid unrealistic outcomes, such as a portfolio concentrated in a single asset, apply constraints. Set minimum and maximum allocation limits for each asset class (e.g., no more than 30% in any single stock).

- Regularly Rebalance: Market movements will cause your portfolio's weights to drift from their optimal targets. Rebalance periodically, perhaps quarterly or annually, to restore the desired asset allocation.

- Incorporate Forward-Looking Views: A key criticism of MPT is its reliance on historical data. Enhance the model by blending historical statistics with forward-looking estimates for returns and risks, a technique often used in the Black-Litterman model.

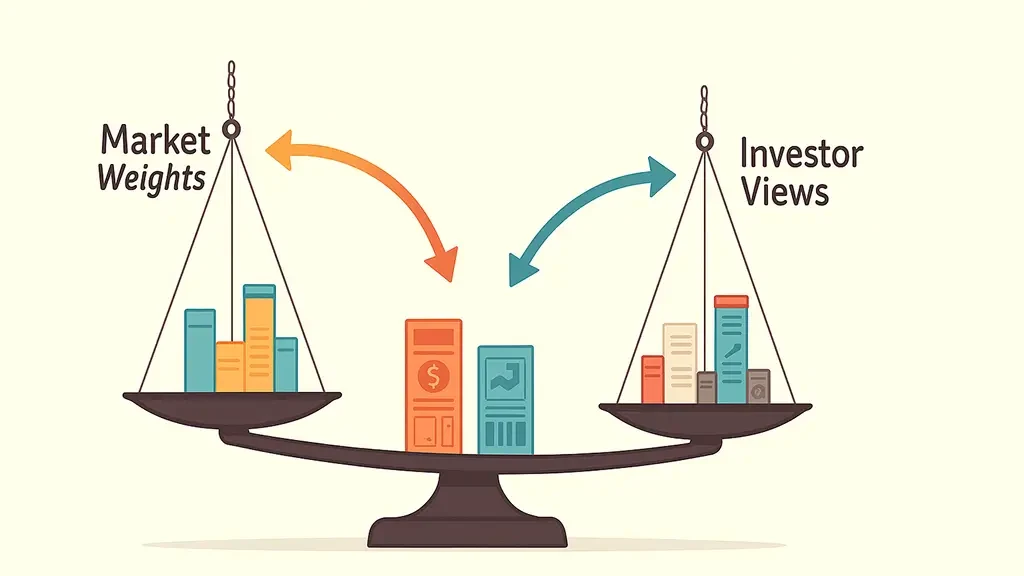

2. Black-Litterman Model

The Black-Litterman Model, developed by Fischer Black and Robert Litterman at Goldman Sachs, is a sophisticated portfolio optimization technique that elegantly addresses a major critique of Modern Portfolio Theory. Instead of relying solely on historical data, it provides a Bayesian framework that blends the market's implied equilibrium returns with an investor's unique, subjective views on future asset performance. This approach produces more stable, intuitive, and diversified portfolio allocations, avoiding the highly concentrated and often impractical results that can emerge from standard mean-variance optimization.

The model's genius lies in its starting point. It assumes the market portfolio is already efficient and calculates the expected returns implied by this equilibrium. An investor can then express specific forecasts (e.g., "I believe tech stocks will outperform utilities by 2%") and a confidence level for each view. The model mathematically combines these views with the market equilibrium, tilting the final portfolio toward the assets the investor favors, with the degree of tilt determined by their stated confidence.

As the diagram illustrates, this method provides a structured way to integrate qualitative expert opinions with quantitative market data, resulting in a more refined asset allocation.

When to Use This Approach

This technique is best suited for institutional investors and sophisticated individuals who have specific market views and want to systematically incorporate them into a well-diversified portfolio. It bridges the gap between purely quantitative models and active management. For example, Goldman Sachs Asset Management and State Street Global Advisors often use Black-Litterman principles to guide their tactical and active ETF strategies, allowing them to adjust allocations based on forward-looking macroeconomic forecasts without abandoning a disciplined framework.

The following summary highlights how this model refines the optimization process by merging market consensus with individual expertise.

Actionable Implementation Steps

To effectively apply the Black-Litterman Model, consider these best practices:

- Start with Simple Views: Begin by incorporating a small number of high-conviction views. For example, express a relative view (e.g., Asset A will outperform Asset B) rather than an absolute one, as these are often more stable.

- Calibrate Confidence Levels Carefully: Your confidence in a view directly impacts its influence on the portfolio. Be realistic and systematic when assigning confidence levels, as overconfidence can lead to excessive risk-taking.

- Use Robust Covariance Estimation: The model's outputs are sensitive to the covariance matrix, which describes how assets move together. Use advanced statistical methods like shrinkage or factor models to get more stable and reliable estimates than historical data alone can provide.

- Validate Results: Always check the model's recommended portfolio against your intuition and current market conditions. If the output seems counterintuitive, re-examine your input views and confidence levels to ensure they accurately reflect your market outlook.

3. Risk Parity

Risk Parity is a portfolio allocation strategy that shifts the focus from capital allocation to risk allocation. Instead of distributing capital equally or based on expected returns, this technique aims to ensure that each asset or asset class contributes equally to the overall portfolio's risk. Popularized by Ray Dalio of Bridgewater Associates, Risk Parity challenges the traditional 60/40 stock-bond portfolio, arguing that it is overwhelmingly dominated by the risk of the equity portion.

This approach operates on the premise that a truly diversified portfolio should be balanced in terms of risk, not just dollars. Since lower-risk assets like bonds have lower volatility, a Risk Parity strategy often uses leverage to increase their position size, bringing their risk contribution up to the level of higher-risk assets like stocks. This method is one of the more advanced portfolio optimization techniques, designed to create a smoother return profile across different economic environments.

As the visualization highlights, the goal is to balance the portfolio so that no single asset class's volatility dominates the portfolio's performance.

When to Use This Approach

Risk Parity is best suited for investors seeking consistent returns and lower volatility, especially those concerned with surviving various economic regimes like inflation, deflation, and changing growth rates. It is particularly effective for those who want to avoid the heavy equity risk concentration found in traditional portfolios. Prominent examples include Bridgewater's renowned All Weather strategy and commercial products like AQR's Risk Parity funds, which have demonstrated the strategy's resilience.

Actionable Implementation Steps

To effectively apply a Risk Parity strategy, consider these key actions:

- Use Multiple Risk Measures: While volatility is the standard metric, enhance your model by incorporating other risk measures like Value at Risk (VaR) or expected shortfall to get a more complete picture of potential downside.

- Monitor Leverage Levels Carefully: Since this strategy often involves leveraging lower-volatility assets, it is crucial to manage leverage prudently. Set strict limits and understand the associated costs and risks, especially during periods of rising interest rates.

- Implement Gradual Transitions: When rebalancing or shifting to a new allocation target, do so gradually. This helps minimize transaction costs and avoids the negative impacts of making large trades based on short-term risk fluctuations.

- Consider Asset Correlations: A core component of risk contribution is how assets correlate with one another. Continuously monitor and update your assumptions about asset correlations, as they can change significantly in different market environments.

4. Factor-Based Optimization

Factor-Based Optimization moves beyond traditional asset classes to construct portfolios based on exposure to specific, systematic risk factors. This is one of the more modern portfolio optimization techniques, popularized by academics like Eugene Fama and Kenneth French. Instead of focusing on individual stocks or bonds, this approach identifies broad, persistent drivers of return such as value, momentum, quality, and low volatility, and then builds a portfolio to strategically target these exposures.

The core idea is that the returns of any diversified portfolio can be explained by its underlying factor exposures. By deliberately tilting a portfolio toward factors that have historically provided a return premium, investors aim to enhance performance beyond what a standard market-cap-weighted index can offer. This technique allows for a more granular and intentional approach to capturing risk premia while managing unintended factor tilts and maintaining overall diversification.

When to Use This Approach

This strategy is best suited for sophisticated investors who want to deconstruct portfolio returns and target specific drivers of performance. It is particularly useful for those looking to outperform broad market benchmarks over the long term by capturing well-documented risk premia. Prominent examples include AQR's factor-based mutual funds and Vanguard's Multifactor ETF series (e.g., VFMF), which are designed to provide investors with diversified exposure to multiple equity factors simultaneously.

This method allows investors to build a portfolio that reflects their specific views on which factors are likely to perform well, moving beyond a simple stock-picking or asset allocation framework.

Actionable Implementation Steps

To effectively implement Factor-Based Optimization, focus on a disciplined and evidence-based process:

- Use Well-Researched Factors: Base your strategy on factors with strong academic evidence of persistence and pervasiveness across different markets and time periods. Avoid chasing recent "hot" factors without robust validation.

- Monitor Factor Loadings Regularly: Your portfolio's exposure to desired factors will drift over time due to market movements. Use analytical tools to monitor your factor loadings and rebalance as needed to maintain your target exposures.

- Consider Factor Interactions: Factors are not independent; their correlations can change, impacting portfolio behavior. For example, value and momentum are often negatively correlated, which can provide a diversification benefit when combined.

- Balance Factor Exposure with Costs: Tilting a portfolio toward specific factors often involves higher turnover and transaction costs compared to passive indexing. Ensure the expected premium from your factor exposure justifies these additional expenses.

5. Minimum Variance Optimization

Minimum Variance Optimization is a specialized portfolio construction method that prioritizes one goal above all others: minimizing portfolio volatility. Unlike Modern Portfolio Theory, which balances risk and return, this approach focuses exclusively on finding the combination of assets with the lowest possible portfolio variance, irrespective of expected returns. This technique is rooted in the observation of the "low-volatility anomaly," where portfolios of low-risk stocks have historically generated surprisingly strong risk-adjusted returns.

The core principle is to leverage the covariance matrix of asset returns to construct the least volatile portfolio possible. Proponents like Choueifaty and Coignard have shown that such portfolios can offer downside protection during market downturns. The strategy often results in a concentration in traditionally stable, low-volatility assets and sectors, such as consumer staples and utilities, making it one of the more conservative portfolio optimization techniques.

When to Use This Approach

This technique is best suited for highly risk-averse investors, such as retirees or those prioritizing capital preservation over aggressive growth. It's an excellent strategy for the defensive portion of a core-satellite portfolio or for investors who want to mitigate downside risk during periods of high market uncertainty. Major asset managers have embraced this concept, with products like the iShares Edge MSCI Min Vol USA ETF (USMV) and indices from MSCI providing real-world examples of its successful implementation.

The following summary box highlights the core components of this risk-focused framework.

As the visualization shows, the primary objective is to build a resilient portfolio by minimizing its overall variance through careful asset selection and weighting.

Actionable Implementation Steps

To effectively apply Minimum Variance Optimization, consider the following best practices:

- Apply Concentration Constraints: To avoid unintentionally concentrating the portfolio in just a few low-volatility assets, set maximum allocation limits for individual securities or sectors. This ensures a baseline level of diversification.

- Use Robust Covariance Estimation: The model's output is highly sensitive to the covariance matrix. Instead of relying solely on historical data, use more advanced statistical methods like shrinkage or factor models to create more stable and forward-looking estimates.

- Monitor Portfolio Turnover: Since the composition of the minimum variance portfolio can change as asset volatilities and correlations shift, it can lead to high turnover. Monitor this closely to manage and control transaction costs.

- Combine with Other Objectives: For a more balanced approach, consider using Minimum Variance as a starting point and then layer on other objectives, such as a minimum expected return threshold, to create a more practical and well-rounded portfolio.

6. Conditional Value at Risk (CVaR) Optimization

Conditional Value at Risk (CVaR) Optimization, also known as Expected Shortfall, is a sophisticated risk management approach that goes beyond traditional measures like standard deviation. It stands out among portfolio optimization techniques by focusing on the severity of losses in the worst-case scenarios. Instead of just identifying a potential loss threshold (like Value at Risk, or VaR), CVaR calculates the average loss that would be incurred if that threshold is breached, giving investors a much clearer picture of tail risk.

Developed by R. Tyrrell Rockafellar and Stanislav Uryasev, this method helps construct portfolios that are not only efficient in terms of return but also resilient during extreme market downturns. By optimizing for CVaR, an investor aims to minimize the expected loss in a "tail" event, such as the worst 5% of possible outcomes. This proactive risk management is crucial for preserving capital during financial crises or black swan events.

When to Use This Approach

CVaR is particularly valuable for risk-conscious investors, hedge funds, and institutional asset managers who prioritize capital preservation and tail risk management. If your primary concern is "what happens if things go very wrong?" then CVaR provides a more comprehensive answer than MPT's variance. It is heavily used by major banks like JPMorgan for risk management and by insurance companies to ensure their asset allocations can withstand catastrophic events. It is also increasingly popular among crypto investors who face extreme volatility and fat-tailed return distributions.

Actionable Implementation Steps

To effectively implement CVaR optimization, consider these best practices:

- Use Multiple Scenarios and Stress Tests: Since CVaR focuses on tail events, its effectiveness depends on accurately modeling potential extreme scenarios. Use historical simulation, Monte Carlo methods, and specific stress tests based on past crises (e.g., the 2008 financial crisis) to generate your return distributions.

- Combine with Other Risk Measures: CVaR provides an excellent view of tail risk but should not be used in isolation. Combine it with measures like standard deviation, Sharpe ratio, or maximum drawdown to get a holistic view of the portfolio's risk-return profile.

- Account for Changing Correlations: During market crises, correlations between assets often converge toward one, reducing diversification benefits when they are needed most. Ensure your model accounts for these conditional correlation shifts.

- Validate Model Assumptions Regularly: The assumptions underpinning your scenarios, especially for alternative assets like crypto, can quickly become outdated. Regularly review and validate your models against new market data to ensure their relevance and accuracy.

7. Maximum Diversification

Maximum Diversification is a sophisticated portfolio optimization technique that aims to construct the most diversified portfolio possible, rather than focusing solely on the trade-off between risk and return. Developed by Yves Choueifaty and Yves Coignard of TOBAM, this approach seeks to maximize the benefits of diversification itself. It operates by maximizing the "Diversification Ratio," which is calculated as the weighted average volatility of individual assets divided by the overall portfolio's volatility.

The core principle is that a higher ratio indicates greater diversification benefits. A portfolio is considered truly diversified not just by holding many assets, but by holding assets that have low correlations with each other, minimizing systemic risk concentration. This method often results in portfolios that differ significantly from market-cap-weighted indices, as it avoids concentrating capital in the largest, most-correlated stocks, which can be a hidden source of risk.

When to Use This Approach

This technique is best suited for investors who prioritize risk management and want to build a portfolio that is resilient to market shocks by avoiding hidden concentrations. It is particularly powerful for those looking to move beyond traditional market-cap weighting and capture diversification alpha. Prominent examples include TOBAM's Anti-Benchmark strategies and various indices from providers like Scientific Beta that are built on maximum diversification principles.

Actionable Implementation Steps

To effectively implement a Maximum Diversification strategy, focus on the following key actions:

- Monitor Correlation Stability: The model's effectiveness hinges on asset correlations. Since correlations can change, especially during market stress, you must monitor them over time and understand their stability.

- Apply Practical Constraints: An unconstrained Maximum Diversification portfolio might lead to heavy allocations in illiquid or obscure assets. Apply practical constraints, such as limits on sector, country, or individual asset weights, to ensure the portfolio remains investable and balanced.

- Understand Low Correlation Drivers: Don't just rely on the numbers. Investigate the fundamental, economic reasons behind low correlations between assets to ensure the diversification is robust and not just a statistical anomaly.

- Combine with Other Objectives: This approach can be blended with other goals. For instance, you can apply a Maximum Diversification framework within a universe of stocks that also meet specific quality or value criteria to create a more robust multi-factor portfolio.

8. Robust Optimization

Robust Optimization is an advanced framework that directly confronts a major weakness in traditional models: their sensitivity to input errors. Standard techniques like Mean-Variance Optimization rely on precise point estimates for expected returns and covariances, but these inputs are notoriously difficult to predict accurately. Robust Optimization addresses this by building portfolios that are resilient to estimation errors, making it one of the more sophisticated portfolio optimization techniques available today.

Developed by pioneers like Dimitris Bertsimas and Arkadi Nemirovski, this approach optimizes a portfolio for the "worst-case" scenario within a defined range of possible input values. Instead of using a single number for an asset's expected return, it uses an "uncertainty set," a range of plausible values. The resulting portfolio is designed to perform reasonably well across all these potential future outcomes, rather than exceptionally well in one specific, and likely incorrect, forecast.

When to Use This Approach

This technique is best suited for institutional investors, quantitative hedge funds, and sophisticated retail investors who recognize the inherent uncertainty in market forecasting. It is particularly valuable during periods of high market volatility or when there is a low conviction in standard model inputs. Academic research from institutions like MIT and its application in risk management systems at firms such as Goldman Sachs highlight its utility in creating portfolios that can better withstand unexpected market shocks and parameter miscalculations.

The following summary box highlights the core components of this advanced framework.

As the visualization shows, Robust Optimization's primary goal is to minimize regret by protecting against unfavorable outcomes stemming from input inaccuracies.

Actionable Implementation Steps

To effectively apply Robust Optimization, consider the following best practices:

- Calibrate Uncertainty Sets: The size and shape of your uncertainty sets are crucial. Calibrate them based on historical parameter instability or statistical confidence intervals to ensure they are realistic without being overly conservative.

- Start with Simple Structures: Begin with basic uncertainty structures, like box or ellipsoidal sets, which are computationally more manageable. This allows you to gain experience with the framework before moving to more complex, custom-defined sets.

- Balance Robustness and Performance: A portfolio that is too robust may be overly defensive and sacrifice too much potential return. Adjust the size of the uncertainty set to find an appropriate balance that aligns with your risk tolerance and return objectives.

- Monitor Cross-Regime Performance: Test and monitor how the robust portfolio performs across different historical and simulated market regimes (e.g., bull markets, bear markets, high-inflation periods) to validate its resilience.

9. Resampled Efficiency (Michaud Optimization)

Resampled Efficiency, often called Michaud Optimization, is a sophisticated enhancement to traditional Mean-Variance Optimization. Developed by Richard and Robert Michaud, this approach directly confronts a key weakness of MPT: its high sensitivity to input estimates. Small changes in expected returns or covariances can lead to drastically different and often unstable optimal portfolios, a problem known as "error maximization." Resampled Efficiency is one of the more advanced portfolio optimization techniques designed to create more robust and stable asset allocations.

The methodology uses Monte Carlo simulation to address this instability. Instead of relying on a single set of historical data, it generates thousands of possible future return scenarios based on the original inputs' statistical properties. An efficient frontier is calculated for each simulated scenario, and the resulting optimal portfolios are then averaged to produce a single, more diversified "resampled efficient" portfolio. This process smooths out the extreme allocations that often arise from single-point estimates.

When to Use This Approach

This technique is best suited for institutional investors and sophisticated advisors who recognize the limitations of classical optimization and seek greater portfolio stability over time. It is particularly valuable when input data is uncertain, which is almost always the case. By building portfolios that are optimal on average across many possible market outcomes, it reduces the need for frequent, reactive rebalancing driven by statistical noise. The investment firm New Frontier Advisors, founded by the Michauds, has built its entire investment process around this methodology, demonstrating its practical application in managing real-world assets.

Actionable Implementation Steps

To effectively apply Resampled Efficiency, focus on building a statistically sound and robust process:

- Ensure Sufficient Simulations: The stability of the final portfolio depends on running a large number of Monte Carlo simulations. A common practice is to use at least 500 to 1,000 iterations to ensure the averaged portfolio accurately reflects the underlying return distributions.

- Validate Input Assumptions: The quality of the simulation depends on the statistical distribution assumed for the inputs. Validate whether the historical data fits a normal distribution or if alternative distributions (like a student's t-distribution with fatter tails) might be more appropriate.

- Monitor Over Multiple Periods: Assess the performance and stability of the resampled portfolio over several rebalancing cycles. The primary benefit is reduced turnover and more consistent allocations, which should become evident over time compared to a standard MVO approach.

- Combine with Other Techniques: While powerful, Resampled Efficiency can be combined with other methods for added robustness. For instance, you could use shrinkage estimators for your covariance matrix before feeding it into the resampling process to further stabilize the inputs.

10. Kelly Criterion Optimization

The Kelly Criterion is a mathematical formula used to determine the optimal size for a series of investments to maximize the long-term growth rate of capital. Originally developed by Bell Labs scientist John Kelly Jr. for information theory and later adapted for gambling by Edward Thorp, it has become a powerful, if aggressive, tool among portfolio optimization techniques. Unlike methods that focus on balancing risk and return, the Kelly Criterion’s sole objective is to maximize the portfolio's compound annual growth rate.

It calculates the optimal fraction of capital to allocate to a single investment based on the probability of success (win rate) and the ratio of potential gain to potential loss (win/loss ratio). The formula essentially advises betting a larger portion of your capital on opportunities with higher perceived edges and positive expected returns. This aggressive approach aims for maximum wealth accumulation over time but comes with significantly higher volatility and drawdown risk compared to more diversified models.

When to Use This Approach

The Kelly Criterion is best suited for active traders, quantitative funds, and sophisticated investors who can accurately estimate the probabilities and payoffs of their investments. It is particularly popular in systematic trading strategies where an edge can be statistically validated. While not a mainstream retail method, its principles are philosophically aligned with how concentrated investors like Warren Buffett approach capital allocation, focusing heavily on their best ideas. Its aggressive nature makes it less suitable for risk-averse or long-term retirement planning.

Some speculate that highly successful quantitative funds, like Renaissance Technologies' Medallion Fund, employ principles derived from or similar to the Kelly Criterion to size their positions and maximize growth.

Actionable Implementation Steps

To apply the Kelly Criterion effectively, a disciplined and analytical approach is crucial:

- Carefully Estimate Probabilities: The model's output is extremely sensitive to your input for win probability and payoff ratios. Use rigorous backtesting or deep fundamental analysis to arrive at realistic estimates.

- Use Fractional Kelly: The full Kelly formula often suggests allocations that are too volatile for most investors. A common practice is to use a "fractional Kelly" (e.g., half-Kelly or quarter-Kelly) to reduce position sizes, which lowers volatility and drawdown risk while still capturing a significant portion of the growth benefit.

- Consider Transaction Costs: The formula does not inherently account for trading commissions or slippage. These costs can erode your "edge," so they must be factored into your win/loss calculations for an accurate optimal position size.

- Monitor Drawdown Tolerance: Be prepared for substantial portfolio drawdowns. Kelly optimization maximizes long-term growth at the expense of short-term stability. Ensure the strategy aligns with your psychological and financial ability to withstand large losses.

Portfolio Optimization Techniques Comparison

From theory to action: Choosing the right optimization technique for you

Navigating the landscape of portfolio optimization techniques can feel like learning a new language. From the foundational principles of Modern Portfolio Theory to the sophisticated risk management of CVaR and the forward-looking views integrated by the Black-Litterman model, the options are as diverse as the investors who use them. We have journeyed through ten distinct methodologies, each offering a unique lens through which to view risk, return, and diversification.

The central takeaway is that there is no universal "best" approach. The true power lies not in blindly adopting a single formula but in understanding the core philosophy behind each one. Your ideal strategy is a deeply personal choice, a reflection of your financial goals, your timeline, your tolerance for volatility, and even your fundamental beliefs about how markets behave.

Synthesizing the Strategies: Key Takeaways

To move from theory to a practical, personalized strategy, it's crucial to distill the primary purpose of each technique.

- For the Foundationalist: If you believe in the classic risk-return tradeoff and seek a balanced, long-term allocation, Modern Portfolio Theory (MPT) and its close relative, Minimum Variance Optimization, provide a solid, time-tested starting point.

- For the Pragmatic Realist: If you acknowledge MPT's limitations with input sensitivity, Resampled Efficiency and Robust Optimization offer powerful ways to build portfolios that are more stable and less susceptible to estimation errors in your data.

- For the Risk-Conscious Planner: If your primary concern is protecting your capital from severe downturns, Conditional Value at Risk (CVaR) and Risk Parity shift the focus from simple volatility to tail risk and balanced risk contribution, creating more resilient portfolios.

- For the Active, Opinionated Investor: If you have strong views on specific assets or market trends, the Black-Litterman Model provides an elegant framework to blend your personal insights with market equilibrium, while the Kelly Criterion offers a disciplined, aggressive approach for those focused on maximizing long-term capital growth.

- For the Diversification Maximizer: If your goal is to build a portfolio where assets work independently, spreading risk as widely as possible, Factor-Based Optimization and Maximum Diversification provide direct routes to achieving that structural integrity.

Your Actionable Next Steps

Mastering these concepts transforms you from a passive investor into an active architect of your financial future. It equips you with the knowledge to ask the right questions and to critically evaluate whether your current allocation truly aligns with your objectives.

- Define Your Philosophy: Before running any numbers, articulate your investment philosophy. Are you primarily concerned with avoiding major losses, maximizing growth, or generating stable income? Your answer will immediately point you toward a specific subset of these models.

- Assess Your Inputs: Remember the "garbage in, garbage out" principle. The quality of your expected returns, volatilities, and correlations is paramount. Spend time researching and refining these inputs, as they are the fuel for any optimization engine.

- Start Simple, Then Layer: You don’t need to implement a complex model from day one. Begin with a foundational approach like MPT or Minimum Variance. Once you are comfortable, you can layer in concepts from other models, such as using CVaR to stress-test your MPT-derived portfolio or using factor analysis to ensure it's truly diversified.

- Embrace Technology: Manually implementing these portfolio optimization techniques is complex and time-consuming. Modern financial platforms are essential for applying these theories with real-world data, running backtests, and stress-testing your assumptions against various market scenarios.

Ultimately, the journey through these portfolio optimization techniques is one of empowerment. It is about moving beyond generic advice and building a sophisticated, data-driven investment process that is meticulously tailored to you. By understanding the 'why' behind each model, you gain the confidence to construct a portfolio designed not just to survive market turbulence, but to thrive in pursuit of your most important financial goals.

Ready to put these powerful theories into practice without the complex spreadsheets? PinkLion provides an intuitive platform that incorporates the principles of advanced portfolio optimization, allowing you to analyze, stress-test, and improve your portfolio with AI-driven insights. Take control of your investment strategy by visiting PinkLion and discover how to build a smarter, more resilient portfolio today.