How to Calculate Dividend Payments Accurately

Learn how to calculate dividend payments with our guide. We cover the formulas, real-world examples, and tools to help you track your investment income.

Figuring out your dividend payment is actually pretty simple. The core formula is just the dividend per share (DPS) multiplied by the number of shares you own. That's it. This quick calculation tells you exactly how much cash a company is about to send your way for being a shareholder.

First, What Exactly Is a Dividend Payment?

Before we get into the math, let's back up a step. A dividend is your slice of a company's profits. When a business does well and has extra cash, its board of directors can decide to share some of that success directly with its owners—the shareholders. That payout is the dividend.

For anyone just getting started, this is a fundamental concept in dividend investing for beginners. It's what turns an abstract stock holding into a real, tangible income stream you can actually plan around.

Key Dividend Terminology Explained

To get your calculations right, you need to know the lingo. There are a few key terms that pop up constantly in the world of dividends. Getting them straight from the start will save you a lot of confusion down the road.

This table breaks down the essential terms you'll encounter.

Understanding these terms makes the whole process click. Once you have them down, the math itself is straightforward.

Let’s run a quick, real-world example. Say a company declares a quarterly dividend of $0.50 per share, and you happen to own 1,000 shares.

Your payment would be $0.50 multiplied by 1,000 shares, which comes out to a neat $500 hitting your account on the payment date.

Mastering these basic terms and the simple formula is all it takes to build a solid foundation for tracking your dividend income. From here, you can start digging into more advanced topics, like the growth trends that experts at J.P. Morgan Asset Management are seeing in the market.

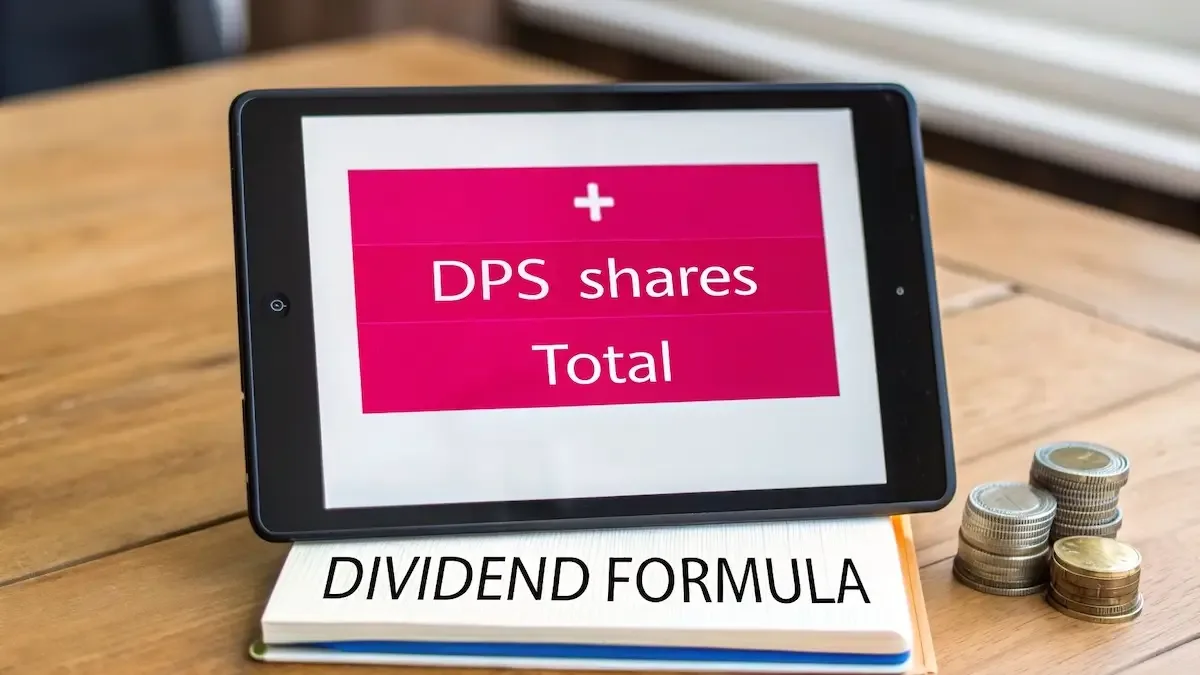

The Core Formulas Every Investor Should Know

Alright, now that we've covered the key terms, it's time to get into the math. Don't worry, it's simpler than you might think. The most fundamental formula for figuring out your payout is refreshingly direct.

All you need are two numbers: the company’s dividend per share (DPS) and how many shares you actually own. That’s it.

Total Dividend Payment = Dividend Per Share (DPS) × Number of Shares Owned

Let's put this into practice. Imagine you own 150 shares of a big-name tech company. They just announced a quarterly dividend of $0.90 per share. Your calculation is simply $0.90 × 150, which gives you $135. That's the cash you can expect to hit your account for the quarter.

Moving Beyond the Basic Payout

Knowing your exact payment is fantastic for planning your cash flow, but there’s another metric that helps you really compare different investment opportunities. This second key formula is for calculating the dividend yield.

In simple terms, dividend yield shows your annual dividend income as a percentage of the stock’s current price. It gives you context.

The formula looks like this:

Dividend Yield = Annual Dividend Per Share ÷ Current Stock Price

A higher yield can signal a stronger return on your investment relative to what you paid for it. But remember, it’s just one piece of the puzzle. It’s also critical to understand what percentage of its earnings a company is paying out. For that, you’ll want to learn how to calculate the dividend payout ratio, as it offers deeper clues into a company's financial health.

Calculating the yield is crucial because it frames the dividend in a way you can easily compare. For instance, a $2.00 annual dividend from a $50 stock gives you a 4% yield. But that same $2.00 dividend from a $100 stock? That's only a 2% yield. This simple percentage makes it much easier to see which stock is working harder for your money.

Putting Dividend Calculations Into Practice

Alright, enough with the theory. Let's get our hands dirty and see how these calculations work in the real world. Putting the formulas to work with a few concrete examples is the best way to make it all click.

We'll start with a classic blue-chip stock, the kind known for its steady-Eddie reliability.

Imagine you own 200 shares of a big industrial company. The board just declared its regular quarterly dividend of $0.75 per share.

The math is straightforward:

200 shares × $0.75/share = $150

Just like that, you know you've got a $150 payment coming your way this quarter. To get a feel for your annual income from this single stock, you'd just multiply that by four. That's $600 for the year, assuming the dividend stays the same. This kind of predictability is exactly why so many investors build their portfolios around these mature, stable companies.

What About a Growth Stock?

Now, let's switch gears and look at a fast-growing tech firm. These companies are often in a different phase of their lifecycle, so they tend to reinvest more of their cash back into the business to fuel expansion. As a result, they might pay dividends less frequently, maybe just twice a year.

Let's say you own 500 shares of a growth stock that pays a semi-annual dividend of $0.40 per share.

The calculation is just as simple:

500 shares × $0.40/share = $200

You'd pocket that $200 payment twice a year, giving you a total of $400 in annual dividend income. The core math doesn't change, but the payment frequency definitely impacts the timing of your cash flow.

To give you a clearer picture, let's compare a few different scenarios side-by-side.

Sample Dividend Payment Scenarios

The table below shows how your quarterly income can vary based on the type of company, its dividend policy, and how many shares you hold.

As you can see, a high-yield stock paid monthly can generate significant quarterly cash flow, while a growth stock might offer a lump-sum payment less frequently. It all depends on the company's strategy.

Some companies have a truly remarkable history of dividend consistency. This kind of track record is often a powerful signal of deep financial strength and disciplined management—it shows a genuine, long-term commitment to rewarding shareholders.

A perfect example is S&P Global. They've paid a dividend every single year since 1937 and are part of an elite group of S&P 500 companies that have increased it for over 50 consecutive years. This doesn't happen by accident; it's the result of a clear dividend policy that's backed by stable earnings and strong cash flow. You can actually explore the dividend history of consistent payers like them to see these powerful patterns for yourself.

Factoring in Dividend Reinvestment

So, what happens if you're not taking the cash? If you're using a Dividend Reinvestment Plan (DRIP), things get even more interesting. This is where the magic of compounding really kicks in.

Let’s jump back to our first example where you received that $150 dividend. If the company's stock is trading at $100 per share on the payment date, your DRIP automatically uses that cash to buy you more shares.

$150 dividend ÷ $100/share = 1.5 additional shares

Your new total holding is now 201.5 shares.

Come next quarter, your dividend payment will be calculated based on this slightly larger share count. It might seem small at first, but over years and decades, this automatic reinvestment process can dramatically accelerate your investment's growth.

Factors That Can Change Your Dividend Payments

Knowing how to calculate a dividend payment is a great starting point, but don't get too comfortable. Your dividend income isn't set in stone. In the real world, several factors can cause those payouts to grow, shrink, or even vanish entirely, so it’s crucial to look beyond a single calculation.

A company's financial health is almost always the main driver. Strong, consistent profits and healthy cash flow often lead to dividend increases—a powerful signal of management's confidence in the future. On the flip side, a period of struggle, declining sales, or unexpected industry headwinds can force a company to make a tough choice.

When Payouts Fluctuate

This is where you might see a dividend cut (a reduction in the dividend per share) or, in more serious cases, a complete dividend suspension. While alarming for income investors, these moves are often made to preserve cash for essential operations during lean times. Remember, a dividend is a choice, not a legal obligation.

A company’s dividend policy is more than just a number; it's a direct message to shareholders about its financial health and long-term priorities. Consistent growth signals stability, while a sudden cut can be a major red flag.

It's not all doom and gloom, though. A company enjoying a windfall from an asset sale or an exceptionally profitable year might issue a special dividend. Think of this as a one-time bonus payment on top of the regular dividend. It’s a smart way to reward shareholders without committing to a permanently higher regular payout. For instance, a company might declare its usual $0.50 quarterly dividend but add a special, one-time $2.00 dividend.

Understanding these dynamics is key to managing your income expectations. Your dividend stream can change due to:

- Company Profitability: Rising profits are the fuel for dividend hikes.

- Economic Conditions: A broad recession can pressure even healthy companies to cut dividends.

- Strategic Decisions: A company might choose to reinvest cash into R&D or an acquisition instead of paying it out.

- Unexpected Windfalls: Asset sales or record profits can lead to those special, one-off payments.

Automate Your Dividend Tracking with PinkLion

Calculating dividends for one or two stocks is simple enough. But once your portfolio grows beyond a handful of holdings, trying to keep track of everything in a spreadsheet becomes a massive headache—and it’s surprisingly easy to make mistakes.

This is where you graduate from manual grunt work to smart automation.

PinkLion’s platform is built to handle all that complexity for you. Instead of wrestling with dates and numbers, you can link your brokerage account or simply add your stocks individually. The system takes it from there, automatically tracking and calculating every dividend payment you're due to receive.

Get Instant Dividend Clarity

Once your portfolio is synced up, you get a crystal-clear view of your income stream. No more guessing games or digging through brokerage statements to find payment dates.

Here’s how our tools make it effortless:

- Automatic Payment Calculation: The platform does all the math, showing you exactly how much cash to expect from each of your holdings.

- Upcoming Dividends Calendar: The visual calendar gives you a clear schedule of when you’ll get paid, making cash flow planning a breeze.

- Portfolio-Wide Totals: See your total projected dividend income for the month, quarter, or year at a single glance.

By automating the tedious parts of portfolio management, you free up valuable time to focus on what truly matters: making informed investment decisions and growing your wealth.

This shift from reactive data entry to proactive financial planning is a game-changer. You can find more tips on getting set up in our guide to using a dividend portfolio calculator.

A Few Common Questions About Dividends

Once you’ve got the formulas down, you’ll find a few practical questions still pop up. I see them all the time. Getting the answers straight helps you build a smarter strategy and sidestep some common headaches.

Here’s what every dividend investor eventually asks.

Are Dividend Payments Guaranteed?

This is a big one. And the short answer is no, dividends are never set in stone.

A company's board of directors has to formally declare each and every payment. If the business hits a rough patch or cash flow gets tight, that same board can vote to reduce the dividend—or even scrap it completely. It happens.

That’s why you’ll see experienced investors gravitate toward companies with a long, steady history of paying and increasing their dividends. It’s a powerful signal of financial health and a management team that truly cares about its shareholders.

How Do I Handle Taxes on My Dividends?

The tax man always gets his cut, but how much can vary quite a bit.

In the U.S., for example, dividends are generally split into two buckets. Qualified dividends get taxed at the much friendlier long-term capital gains rates. On the other hand, non-qualified dividends are taxed at your regular income tax rate, which is usually higher.

My favorite way to sidestep the dividend tax headache? Hold your dividend stocks inside a tax-advantaged account like a Roth IRA. In there, your dividends can grow and compound year after year, completely tax-free.

Whether a dividend is "qualified" depends on things like how long you've held the stock and the type of company it is. The rules can get a little tricky, so it's always smart to run things by a tax professional to make sure you know exactly where you stand.

What’s a Dividend Reinvestment Plan (DRIP)?

A Dividend Reinvestment Plan, or DRIP, is one of the most powerful, hands-off ways to build wealth over time.

Instead of getting your dividend payments as cash in your account, a DRIP automatically uses that money to buy more shares of the same stock—often fractional shares.

This is where the magic of compounding really kicks in. Those new shares you just bought will start earning their own dividends, which then buy even more shares. Over the years, this cycle can dramatically speed up the growth of your investment without you lifting a finger.

Stop calculating and start analyzing. PinkLion automatically tracks your dividends, forecasts your income, and gives you the clarity to make smarter investment decisions. Start for free and see your full dividend picture at PinkLion.